Determining lost-profits damages presents a unique set of challenges. Recovery can potentially fail if the expert lacks basic understanding of the legal principles governing lost profits or the attorney lacks basic understanding of the principles governing their computation. This article explains the fundamentals of lost-profits damages and enumerates some of the considerations that must be taken into account when seeking recovery of these types of damages.

Determining lost-profits damages presents a unique set of challenges. Recovery can potentially fail if the expert lacks basic understanding of the legal principles governing lost profits or the attorney lacks basic understanding of the principles governing their computation. This article explains the fundamentals of lost-profits damages and enumerates some of the considerations that must be taken into account when seeking recovery of these types of damages.

Lost Profits Defined

Fundamentally, lost profits are a form of compensatory damages. They return the injured party to the position in which it would have been had the alleged tort or breach (that is, the harm) not occurred. In this case, the position pertains to profits generated. Lost-profits damages are the difference between the profits the plaintiff would have made if not for the harm, minus the profit the plaintiff actually made during the damages period.

As an example of when lost profits might be appropriate, imagine ABC sells widgets to XYZ. One day, while working on ABC’s manufacturing equipment, Engineering Co. negligently breaks one of ABC’s most important machines. ABC can no longer produce the number of widgets XYZ needs, and XYZ stops ordering from ABC. ABC must buy a new machine, and it has lost a lucrative contract. Assuming certain factors are present, Engineering Co. could be liable to ABC for the profits ABC did not earn because of losing XYZ as a customer.

Certain types of claims are more likely than others to give rise to lost-profits damages. Common claims include an intentional tort such as tortious interference, negligence such as in the example above, or breach of contract. Obviously, given that profits are involved, these types of damages arise when the plaintiff is a type of business or revenue-generating entity. The plaintiff could be anything from a sole proprietorship to a nonprofit organization1 to a Fortune 500 corporation.

Scott Shaffer, CPA, MBA, CFE, is the Wisconsin practice leader for forensic and valuation services at Grant Thornton LLP. He specializes in litigation matters requiring damage computations and forensic accounting expertise. He is a member of the American Institute of Certified Public Accountants, Illinois CPA Society, and the Association of Certified Fraud Examiners and an associate member of the American Bar Association (ABA).

Scott Shaffer, CPA, MBA, CFE, is the Wisconsin practice leader for forensic and valuation services at Grant Thornton LLP. He specializes in litigation matters requiring damage computations and forensic accounting expertise. He is a member of the American Institute of Certified Public Accountants, Illinois CPA Society, and the Association of Certified Fraud Examiners and an associate member of the American Bar Association (ABA).

Brandon Greger, JD, MBA, CFE, is a forensic, investigative, and dispute services associate with Grant Thornton LLP in Chicago. His experience includes litigation support, damage calculations, investigations, and fraud risk and security assessments. He is a member of the ABA, Washington State Bar Association, Chicago Bar Association, and the Association of Certified Fraud Examiners and a graduate of the University of Washington and Loyola University-Chicago.

Brandon Greger, JD, MBA, CFE, is a forensic, investigative, and dispute services associate with Grant Thornton LLP in Chicago. His experience includes litigation support, damage calculations, investigations, and fraud risk and security assessments. He is a member of the ABA, Washington State Bar Association, Chicago Bar Association, and the Association of Certified Fraud Examiners and a graduate of the University of Washington and Loyola University-Chicago.

The Legal Principles of Lost-Profits Damages

Four major legal principles govern recovery of lost-profits damages.

Proximate Cause. First, the injury must have been proximately caused by the harm. While proximate cause should already be a familiar concept, certain considerations are specific to lost-profits cases. For instance, the concept of proximate cause (along with foreseeability) has been held in some jurisdictions to bar certain plaintiffs, such as unestablished businesses,2 from recovering lost-profits damages.

Additionally, courts have taken different views on whether a simple “but for” analysis with regard to the transaction, as opposed to the actual loss, will suffice in certain situations. For example, say a plaintiff was able to show that but for a fraudulent misrepresentation, it would not have entered into an unprofitable transaction. However, if that plaintiff cannot show that absent the misrepresentation it would have actually generated more profit, some jurisdictions may not allow lost-profits damages.3 Attorneys on both sides of the aisle should be aware of the precedent in their jurisdiction regarding the showing of proximate cause required for a recovery of lost profits.

Reasonable Certainty. The second legal principle to consider is proving damages with reasonable certainty.4 Of the courts that have taken the time to explain reasonable certainty, most have stated that this threshold applies to the fact of damages rather than the amount.5 Put another way, it must be shown with reasonable certainty that some profits would have been made. The extent of those profits need not be as certain. That said, the Restatement (Second) of Contracts states that “damages are not recoverable for loss beyond an amount that the evidence permits to be established with reasonable certainty.”6 Attorneys should be aware of their jurisdiction’s application of the reasonable certainty rule with regard to the fact versus amount of damages.

Foreseeability. The third major principle is foreseeability. Most law students study Hadley v. Baxendale in first-year contracts, and attorneys can rest assured that in most jurisdictions the objective “contemplation of the parties” test still reigns.7 In such jurisdictions, lost-profits damages are allowed when it can be reasonably assumed that lost profits as a result of a breach were within the contemplation of the parties when the contract was formed.8

Some jurisdictions have applied the subjective test, requiring that lost-profits damages actually were foreseen by the parties, for example by way of a specific discussion between the parties during contract negotiations. This test is also sometimes applied as an alternative to the Hadley test in situations involving collateral contracts (contracts that are one step removed from the breach or contingent on the breached contract).9

Duty to Mitigate Damages. Finally, an important consideration for defense attorneys is the plaintiff’s duty to mitigate damages. The plaintiff must act reasonably to mitigate lost-profits damages, but the defendant has the burden of proving the plaintiff’s failure to do so. A plaintiff may not, after being injured, simply throw up its hands, close its business, and subsequently sue for the value of all future profits that might have been earned by the business. If this type of claim is made, it is up to the defense to show the failure of the plaintiff to act reasonably to limit the injury to the business’s profits. Additionally, if the plaintiff took steps to mitigate damages, yet the damages claim is for the entirety of profits that might have been earned, it is up to the defense to show the amount of mitigation and to argue for offsetting the damages by that amount.10

Calculating Damages

Once the legal basis for a lost-profits claim is satisfied, focus shifts to the calculation of damages. Fundamental misunderstandings of the lost-profits concept are not uncommon, and thus a thorough grounding in the proper application of lost-profits damages can provide an important advantage to an attorney.

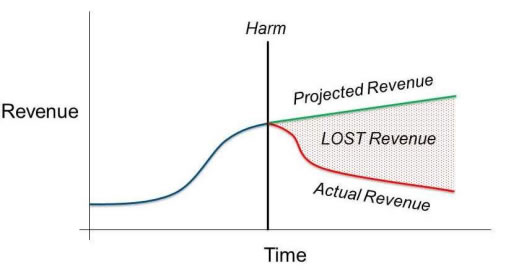

Figure 1

Before & After (B & A) Method

Company A’s Pre-Harm Revenue Trend = +3% Annually

Harm Occurs Jan. 1 Year 1

Projected Year 1 Revenue = Year 0 Revenue x Pre-Harm Trend

= $1 million + 3% = $1.03 million

Actual Year 1 Revenue = $900,000

Company A Year 1 Lost Revenue = Projected Year 1 Revenue – Actual Year 1 Revenue

= $1.03 million - $900,000 = $130,000

Determining the amount of damages generally has three components: determining lost revenue, determining the costs that would have been associated with generating that revenue (resulting in lost profits), and discounting the lost profits to account for time value and risk.

Calculating Lost Revenue. An expert may take several factors into account when determining the amount of revenue a business should have generated were it not for the alleged harm. Generally these include internal factors, such as sales history, and external factors, such as macroeconomic conditions.

Two methods offer common and straightforward applications of these factors. The first is the before and after method (B&A). B&A generally assumes that all trends present at the time of the breach (for example, 3 percent sales growth annually) would have continued were it not for the harm. That trend is then extrapolated over the damages period in question (for example, five years), yielding the projected revenues for the years after the breach. To determine the lost revenue, the amount of revenue actually earned by the plaintiff during the five years after the breach is subtracted from the five-year projection that was made assuming 3 percent annual growth. The difference between these two numbers represents the revenue lost as a result of the breach. [See Figure 1: Before & After (B&A) Method.]

B&A has pros and cons. The method is simple and logical, and projections are based on observed fact, for example, sales history. However, it can be seen as overly optimistic or pessimistic. Similarly, the method can be seen as simplistic and only applicable to businesses with linear revenue trends. Financial performance is often far more volatile, and trends may be more exponential in the case of younger or growing businesses. Using B&A in such situations could prove difficult.

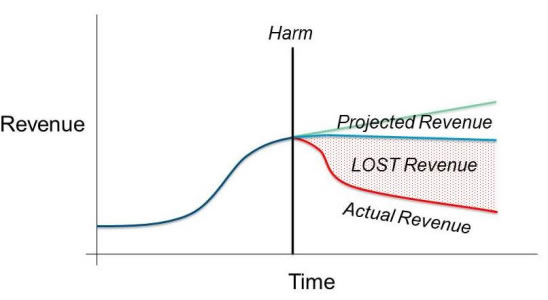

The second common method for determining lost revenue is the industry benchmark or yardstick method. This method assumes the plaintiff’s post-breach performance would mirror that of the plaintiff’s industry generally. Thus, the expert’s selection of the appropriate industry and application of that industry’s trends to the plaintiff’s business are extremely important. For example, say the plaintiff had been experiencing a 3 percent annual increase in sales during the years leading up to the breach, while the industry average was 2.5 percent. Then, six months after the breach, an economic event occurred that drastically reduced demand for the industry’s products. Industry sales growth then decreased by 0.5 percent annually for the following 4.5 years. The yardstick method would project the plaintiff’s post-breach revenues by using the 2.5 percent annual increase for the first six months and 0.5 percent decrease for subsequent years. The plaintiff’s internal trend of 3 percent annual growth is ignored. Once the projection is complete, the calculation of lost revenue is the same as with B&A, in that actual revenue is subtracted from the projected revenue, leaving lost revenue. [See Figure 2: Industry Benchmark or Yardstick Method.]

Figure 2

Industry Benchmark or Yardstick Method

Industry A’s Pre-Harm Trend = +2.5% Annually

Harm Occurs Jan. 1 Year 1

Economic Event Occurs July 1 Year 1, New Industry A Trend = -0.5% Annually

Projected Year 1 Revenue = Company A’s Year 0 Revenue x Industry Trends

$1 million + 2.5% (6 months) - 0.5% (6 months) = $1.0074 million

Actual Year 1 Revenue = $900,000

Company A Year 1 Lost Revenue = $1.0074 million - $900,000 = $107,400

The yardstick method also has strengths and weaknesses. It is a straightforward way to take into account market conditions without applying complex adjustments to a single business. It also uses real data, pulled from industry participants rather than the plaintiff, to arrive at a particular growth metric.

However, it is entirely possible the plaintiff has performed significantly better than the industry average during the past few years. Similarly, it could be difficult to tell how the plaintiff would react to the same changes in market conditions as the rest of the industry. The yardstick method also assumes there is an appropriate industry average, when it is possible that the plaintiff is somehow unique. In the end, it will be up to the expert to determine which method is most appropriate, and of course which adjustments must be made to arrive at a reasonable estimation of the plaintiff’s lost revenue.

Calculating Incremental Costs. After determining the amount of lost revenue, the incremental (sometimes called “avoided”) costs of generating that revenue must be determined. Without determining the cost of generating revenue, one cannot determine the financial state in which the plaintiff would have been if not for the harm.11

Those costs tied directly to the lost revenue may differ from total costs. For example, if the damages period is only one or two years, fixed costs are unlikely to change on account of the harm. If a tort causes the plaintiff to lose out on a business opportunity in the form of a contract with a new customer, it is unlikely the plaintiff would have paid additional rent if not for the breach. The plaintiff’s fixed costs would have remained constant.

Variable costs, on the other hand, very well might have changed. If the plaintiff had to generate more products to fulfill the contract with the new customer, it would have incurred costs of goods sold, as well as sales commissions or marketing costs.

For example, assume the plaintiff historically spent 45 percent of a product’s sale price on production costs. If this were the only incremental cost, the plaintiff’s lost profits would be equal to the remaining 55 percent of revenue lost as a result of the alleged harm. However, in the event the damages period is long, it might be appropriate for the incremental costs to include a percentage of fixed costs. The expert may use any number of methods to determine which costs are appropriately associated with the lost revenue.

Interest and Discounts. Once a lost-profits figure has been determined, it must be adjusted for the time value of money to yield a damages figure that can be paid today.12 These adjustments have two components. First is the interest on the damages that were incurred before the payment of damages. If the breach occurred on January 1, year 1, and the defendant is now paying the damages on January 1, year 2, the interest for that year must be paid to place the plaintiff in the position in which it would have been but for the breach. The injured party would have not only possessed those lost profits but been able to earn interest on those profits. If the lost profit for year 1 was $100, and the simple interest rate was 7 percent, the amount of damages that should be paid on January 1, year 2 would be $107 ($100 in profits + $7 in interest).

The second adjustment is for lost profits that would have been earned in the future. If the breach occurred on January 1, year 1, but that breach affects revenues through January 1, year 5, the cash flows that would have been earned after today (January 1, year 2) must be discounted so that the defendant pays only the present value of those damages. The discount on future cash flows accounts for the time value of money as well as risk adjustments.

Evidence in Lost-Profits Cases

Given these considerations, an expert will need to take into account, at a minimum, the following types of information:

- Historical financial information

- Industry or comparable business information and financials

- Time period of damages (fixed versus indefinite)

- Plaintiff’s cost of capital and capital structure

- Prejudgment interest rate for relevant jurisdiction

- Information regarding business activity, trends, and changes

Common Missteps in Calculating Lost Profits

There are several ways an expert or an attorney could make a mistake when pursuing lost-profits damages. Knowing about these risks increases your proficiency in pursuing lost profits (for a plaintiff) and in rebutting damages claims (for a defendant).

Some errors arise out of faulty or insufficient data. Conclusions regarding damages may be overly speculative regarding rates of growth. Projections may have little underlying support or fail to take into account considerations such as the life cycle of a product (for example, new with growing sales versus mature with waning sales). Growth projections might also fail to take into account the business’s production capacity.

Additionally, miscalculations or misapplications of calculation methods are common in certain areas. For instance, one side may fail to include the interest for historic damages or to discount future damages. Incremental expenses may be misapplied in that all costs are deducted, rather than just those associated with the revenue lost. Also common is a failure to deduct any costs at all, resulting in a damages figure that is purely lost revenue rather than lost profits. Using lost revenues places a plaintiff in a position far superior to the position in which it would have been had the breach not occurred.

Conclusion

A fundamental understanding of these concepts can be the difference between an impeached witness and an educated, successful pursuit of lost-profits damages. With the legal requirements of a claim met, an understanding of the damages calculations and the evidence necessary to support those calculations may offer a distinct advantage to an attorney and client in pursuing or defending a lost-profits claim.

Endnotes

1 American Baptist Churches of Metro. N.Y. v. Galloway, 710 N.Y.S.2d 12 (App. Div. 2000).

2 Robert Dunn, Recovery of Damages for Lost Profits 374 (6th ed. Lawpress Corp. 2005); Stuart Park Assocs. Ltd. P’ship v. Ameritech Pension Trust, 51 F.3d 1319, 1328 (7th Cir. 1995); Roseland v. Phister Mfg. Co., 125 F.2d 417, 420 (7th Cir. 1942).

3 Dunn, supra note 2, at 7; Movitz v. First Nat’l Bank of Chicago, 148 F.3d 760, 765 (7th Cir. 1998).

4 Energy Capital Corp. v. United States, 302 F.3d 1314 (Fed. Cir. 2002).

5 Dunn, supra note 2, at 25; Mid-America Tablewares Inc. v. Mogi Trading Co., 100 F.3d 1353 (7th Cir. 1996).

6 Restatement (Second) Contracts § 352 (1981).

7 Dunn, supra note 2, at 39; Linc Equip. Servs. Inc. v. Signal Medical Servs. Inc., 319 F.3d 288, 289 (7th Cir. 2003).

8 Id.

9 Dunn, supra note 2, at 67.

10 Id. at 569-72.

11 Id. at 469; Magestro v. North Star Environmental Constr., 2002 WI App 182, ¶¶ 14-15, 256 Wis. 2d 744, 649 N.W.2d 722.

12 Dunn, supra note 2, at 541; Bridgkort Racquet Club Inc. v. University Bank, 85 Wis. 2d 706, 271 N.W.2d 165 (Ct. App. 1978).